1 Reports

1.1 Economic

Development Strategy

Author: Paul Numan, General Manager Corporate Services

Authoriser: Angela Oosthuizen, Acting Chief Executive

Attachments: 1. Mackenzie District Council

Economic Development Strategy ⇩

Council

Role:

|

☐ Advocacy

|

When Council or Committee advocates on

its own behalf or on behalf of its community to another level of

government/body/agency.

|

|

☐ Executive

|

The substantial direction setting and

oversight role of the Council or Committee e.g. adopting plans and reports,

accepting tenders, directing operations, setting and amending budgets.

|

|

☒ Legislative

|

Includes adopting District Plans and plan

changes, bylaws and policies.

|

|

☐ Review

|

When Council or Committee reviews

decisions made by officers.

|

|

☐ Quasi-judicial

|

When Council determines an

application/matter that directly affects a person’s rights and

interests. The judicial character arises from the obligation to abide

by the principles of natural justice, e.g. resource consent or planning

applications or objections, consents or other permits/licences (e.g. under

Health Act, Dog Control Act) and other decisions that may be appealable to

the Court including the Environment Court.

|

|

☐ Not applicable

|

(Not applicable to Community Boards).

|

Purpose of Report

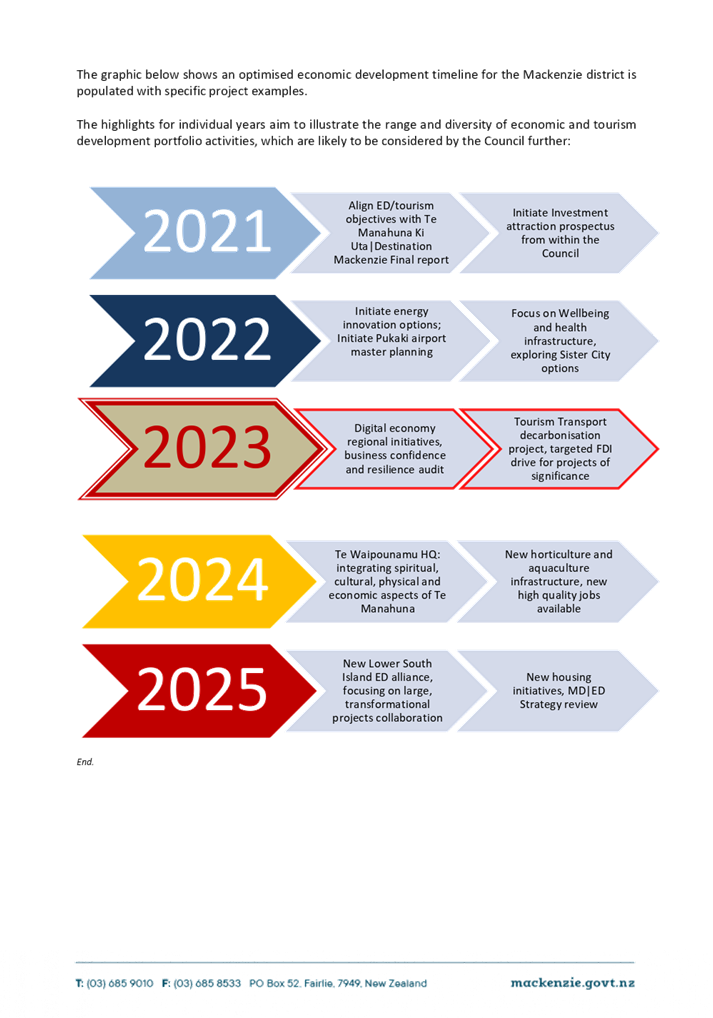

The purpose of this report is to present

the Mackenzie District Council Economic Development Strategy for adoption. The strategy document outlines the Mackenzie District

Council’s vision that the District has a sustainable economic development

with shared access to prosperity, resilient communities and a proud identity.

|

Staff Recommendations

1. That

the report be received.

|

|

2. That the Economic

Development Strategy be adopted by Council.

|

Background

The Economic

Development Strategy sets out the criteria the Council uses to guide decision

making involving the Districts economic and business sector development. The

strategy ensures the reasons behind the Council’s decisions are

consistent, predictable, equitable, and available to the public.

The Economic

Development Strategy is a non-statutory enabling mechanism for Council to

deliver wide spectrum access to prosperity in conjunction with Council’s

other strategic planning instruments such as Te Manahuna Ki Uta | Destination

Mackenzie, Spatial Plan, Long Term Plan and the Te Manahuna Land Strategy.

|

As such, the Economic

Development Strategy is a key tool to enable optimal access to prosperity by

the Mackenzie District community.

|

Policy Status

The Economic Development Strategy is now

submitted to Council for approval.

Significance of Decision

In accordance with the Council's

Significance and Engagement Policy, adoption of this Strategy has been assessed

as having low significance and will not require community consultation.

Options

N/A

Considerations

Legal

N/A

Financial

N/A

Other

N/A

Conclusion

It is recommended that the Council adopt

the attached Economic Development Strategy.

1.2 Rates

Resolution - section 50 of the Local Government (Rating) Act 2002

Author: Paul Numan, General Manager Corporate Services

Authoriser: Angela Oosthuizen, Acting Chief Executive

Attachments: Nil

Council

Role:

|

☐ Advocacy

|

When Council or Committee advocates on

its own behalf or on behalf of its community to another level of

government/body/agency.

|

|

☐ Executive

|

The substantial direction setting and

oversight role of the Council or Committee e.g. adopting plans and reports,

accepting tenders, directing operations, setting and amending budgets.

|

|

☒ Legislative

|

Includes adopting District Plans and plan

changes, bylaws and policies.

|

|

☐ Review

|

When Council or Committee reviews

decisions made by officers.

|

|

☐ Quasi-judicial

|

When Council determines an

application/matter that directly affects a person’s rights and

interests. The judicial character arises from the obligation to abide

by the principles of natural justice, e.g. resource consent or planning

applications or objections, consents or other permits/licences (e.g. under

Health Act, Dog Control Act) and other decisions that may be appealable to

the Court including the Environment Court.

|

|

☐ Not applicable

|

(Not applicable to Community Boards).

|

Purpose of Report

The purpose of this report is to meet the

requirements of Section 50 of the Local Government (Rating) Act 2002 which

states that Council may deliver a rates invoice for not more than 25% of the

rates payable in the previous year if it is not able to deliver a rates

assessment at least 14 days before:

a) The date on which the first

instalment of rates for the current year is payable in a case where the rates

have been set by resolution of the local authority under section 23 of the

Local Government (Rating) Act 2002, or

b) The date one calendar year

after the date when the first payment of rates for the previous year was

payable in a case where no resolution has been made under Section 23 of the

Local Government (Rating) Act.

|

Staff Recommendations

1. That the report be

received.

2. That the Mackenzie District

Council resolves to deliver a rates invoice for 25% of the rates that are

payable in the previous year.

3. That the due dates of the

rates invoice is 20 September 2021

4. That pursuant to sections

57 of the local Government (Rating) Act 2002, the Council prescribes the

following penalty be added to unpaid rates:

A penalty of

10% will be added to unpaid rates from previous financial years unpaid on the

later of 5 working days after the date of the resolution or 3 August 2021.

The penalty charge will be applied on so much of any rates levied before 1

July 2021 which remain unpaid on 3 August 2021.

|

Background

Section 50 of the Local Government (Rating)

Act covers the delivery of a rates invoice for 25% of the rates that are

payable in the previous year.

Policy Status

Not applicable.

Significance of Decision

This matter is deemed significant under the

Council’s Significance Policy as the setting of the rates is a material

revenue source and the alternative procedure being used although provided for

by the Act is due to a statutory breach in not adopting the Long-Term Plan timeously

as required by the Local Government Act. No consultation is required under the

alternative procedure defined in Section 50 of the Rating Act.

Options

Council has two options:

a) Deliver a rates invoice for

on 25% of the rates that are payable in the previous year by passing the above

resolution as set out in recommendation 2. This is deemed to be the preferred

option as it ensures that we generate cash flow (albeit at a reduced level) to

meet Council’s operating requirements.

b) Not pass the above resolution

as recommended and assess the rates payable in three instalments. This would

mean ratepayers would need to pay higher rates instalments over 3 instalments

instead of 4. This would be confusing to Ratepayers expecting a rates invoice

in August (payable in September) and this could prove to be onerous and create

financial hardship for some ratepayers.

Considerations

Administrative provisions

· Arrears penalties

will be authorised (to rates unpaid from previous years) by the Council, by

resolution in the normal way.

· Penalties on unpaid

section 50 rates will not be levied

· Rates set under

section 50 will be based on last year’s rates assessment (ie 25% of the

amount assessed last year) regardless of any changes in valuations.

· No funding impact

statement is required to be set as the rates are based on last year’s

rates

· The invoice is

delivered to the ratepayer in the normal way.

· As provided for in

section 50 of the Rating Act is limited to those rating units that were

actually assessed for rates in the previous financial year. To the extent that

ratepayers have changed (e.g. through the sale of a rating unit), then the

invoice will be sent to the current ratepayer.

· Ratepayers who pay

the 25% invoice will end up having paid an amount that will be taken into

account when the Council has resolved to set and assess the rates. When

assessing the 2021/2022 rates on rating units that have paid the section 50

rates, the amount due will show as a credit and reduce the rates payable.

· New rating units

(for example, created through subdivision) will obviously have the full amount

of the 2021/22 rates payable over the 3 instalments with no reduction to

reflect the section 50 rates (because those rating units will not have been

invoiced under section 50).

Legal

Legal advice on this matter has been

provided by Simpson Grierson and is attached in public excluded.

Section 50 of the Local Government (Rating)

Act is the only option available if Council wish to provide a rates invoice

before the LTP process has been completed.

Financial

If Council chooses not to invoice rates by

Section 50, there will be cashflow implications for the day-to-day operations

of the Council. The amount of the reduced cash flow would be

approximately $3.8M (comprising 25% of the total of the

previous years rates) and that $604K would be the ECan portion. Council would ensure that adequate funding is available by

utilisation of investments.

Conclusion

That Council adopts the staff

recommendation 2 and 3.

By applying Section 50 of the Local Government

(Rating) Act to send out a rates invoice is the only method whereas Council can

keep the status quo in sending out 4 rates invoices to its ratepayers for this

financial year 1 July 2021 to 30 June 2022. This is the fairest way to spread

the cost of the annual rates to its ratepayers.